- About Us

- Our Services

- Your Industry

- Resources

- News & Blog

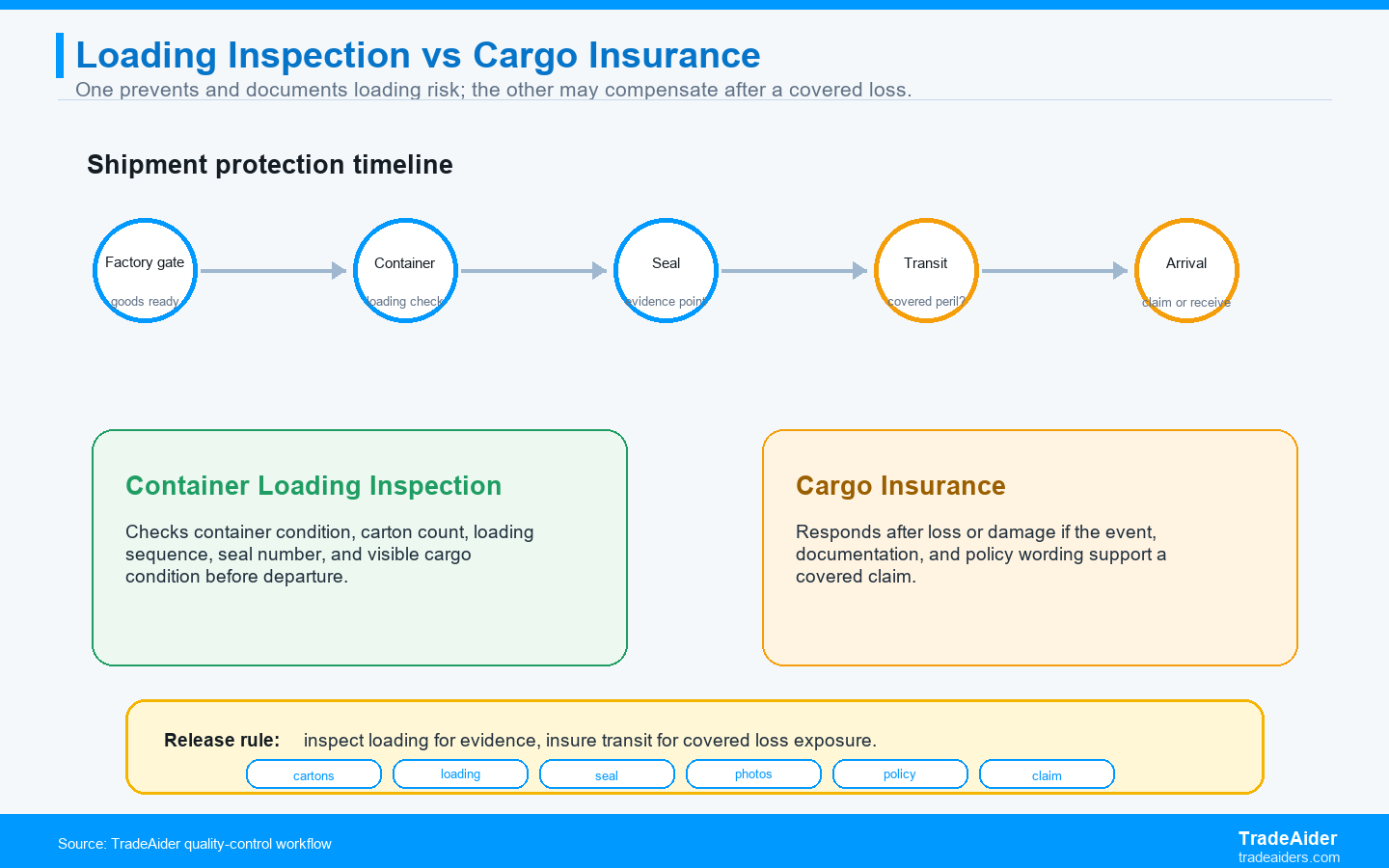

Container loading inspection protects quality in transit by preventing and documenting loading errors before departure, while cargo insurance protects financial recovery only after a covered loss or damage event is proven under the policy. They are complementary controls, not substitutes.

Importers often ask whether they need container loading inspection if they already buy cargo insurance. The question sounds logical because both relate to shipment risk. But they solve different problems. Loading inspection is a prevention and evidence tool. Cargo insurance is a financial recovery tool after something goes wrong.

A container loading inspection can check whether the right goods are loaded, whether cartons are visibly damaged before loading, whether the container is clean and suitable, whether loading follows the plan, whether quantities match documents, and whether the seal number is recorded. Cargo insurance does not perform those checks. It may respond later if a covered transit loss occurs and the buyer has enough documentation.

This article is practical guidance for importers, not legal or insurance advice. Policy wording, Incoterms, exclusions, claim procedure, and local law matter. Buyers should review coverage with their broker, forwarder, and counsel where necessary.

The Direct Answer

Use container loading inspection to prevent and document loading risk; use cargo insurance to finance recovery from covered transit loss.

The International Chamber of Commerce's Incoterms 2020 rules explain that CIF and CIP include seller insurance obligations with different coverage levels. That matters because some buyers hear "insurance included" and assume the shipment is fully protected. Incoterms allocate responsibilities and, in CIF or CIP, require certain insurance arrangements; they do not inspect the container, prove carton condition, or fix poor loading.

TradeAider's container loading supervision content describes loading supervision as oversight of goods being loaded and secured into shipping containers, including container inspection, packaging review, and verification against agreed terms. That is the evidence layer cargo insurance cannot create after the fact.

Container Loading Inspection vs Cargo Insurance

One creates pre-departure evidence; the other depends on post-loss proof.

| Factor | Container Loading Inspection | Cargo Insurance |

|---|---|---|

| Primary purpose | Prevent and document loading errors before departure | Provide financial recovery after a covered loss |

| Timing | At factory or warehouse during container loading | After loss, damage, or claim event |

| Controls quality | Controls visible loading, quantity, carton, and seal evidence | Does not control product quality or loading execution |

| Evidence created | Photos, videos, carton count, container condition, seal number | Claim file, policy, survey, transport documents, proof of loss |

| Best for | Wrong goods, carton damage before loading, poor loading sequence, missing seal evidence | Covered transit damage, loss, theft, or insured peril depending on wording |

| Weakness | Cannot compensate after an insured loss by itself | May not cover factory defects, poor packing, delay, or excluded causes |

The strongest transit protection combines loading evidence before departure with insurance for covered loss after departure.

What Container Loading Inspection Checks

Loading inspection protects the handoff point where accepted goods become cargo in transit.

A practical loading inspection checks container condition before loading: cleanliness, odor, holes, water marks, floor condition, door function, and suitability for the cargo. It checks whether carton condition is acceptable before cartons enter the container. It verifies loading quantity, carton marks, pallet or non-pallet loading method, loading sequence, visible damage, and seal number.

The inspection can also check whether the loaded goods match the shipment approved by PSI. This matters when a factory has multiple orders, similar cartons, mixed SKUs, or split batches. The buyer wants evidence that the accepted lot, not a substituted or mixed lot, entered the container.

Loading supervision is not a replacement for PSI. PSI checks product quality before release. Loading inspection checks the loading event after product acceptance. If the buyer skipped PSI, loading inspection may confirm that cartons were loaded, but it cannot fully prove product workmanship, function, labeling, or AQL acceptance inside the cartons.

What Cargo Insurance Does And Does Not Do

Cargo insurance can help recover money, but it does not create quality control.

Cargo insurance may respond when goods are lost or damaged by a covered event during transit, subject to the policy wording, insured value, exclusions, documents, and claim process. It is important because international transit has real risks: rough handling, water exposure, theft, vessel incidents, container damage, and other events that may be outside the buyer's direct control.

Insurance does not prevent a factory from loading the wrong SKU. It does not confirm carton count at origin. It does not verify that the container was clean before loading. It does not prove whether cartons were already crushed before departure. It does not normally solve ordinary quality defects, wrong labels, poor workmanship, unsupported compliance claims, or factory-caused packing problems.

Insurance also depends on evidence. If the buyer cannot show pre-loading condition, loaded quantity, seal number, transport records, arrival condition, and timely claim documents, recovery can become harder. Loading inspection helps create the origin-side evidence that a later claim or dispute may need.

The Evidence File A Buyer Should Keep

The strongest transit protection file starts before loading and ends after receiving.

Before loading, keep the PSI report, packing list, carton count, SKU breakdown, accepted corrective-action records, and loading appointment details. During loading, keep container photos, empty-container condition photos, carton-condition photos, loading sequence photos or video, final loaded-container view, seal number, truck or container number, and inspector notes.

After departure, keep the bill of lading, commercial invoice, packing list, insurance certificate, freight documents, tracking records, and any carrier notices. At arrival, photograph container seal condition, door opening, carton condition, pallet condition, visible water marks, shortages, and damaged units before moving goods deeper into the warehouse.

This file is useful even if no insurance claim is filed. It helps the buyer understand where the problem likely occurred: factory packing, loading, carrier handling, transit, destination unloading, or warehouse receiving. Without a timeline of evidence, every party can blame another part of the chain.

Why Incoterms Matter But Do Not Replace Inspection

Incoterms define responsibilities, not shipment quality.

Under Incoterms 2020, insurance obligations appear specifically under CIF and CIP, and the ICC notes that different levels of insurance coverage apply to those rules. That is useful for contract planning, but buyers still need to know when risk transfers, who arranges transport, what insurance level applies, and whether the coverage matches the real cargo risk.

For example, a buyer purchasing under CIF may assume the seller's insurance is enough. But the seller may arrange only the required level, and the buyer may still need broader coverage, better claim documents, or separate protection. The buyer should not confuse "insurance arranged" with "quality protected."

Loading inspection sits outside the Incoterms label. Whether the trade term is FOB, FCA, CIF, CIP, or another term, the buyer still benefits from knowing what was loaded, in what condition, in what quantity, and under which seal.

Common False Assumptions About Transit Protection

Most transit-protection mistakes come from assuming one document covers every risk.

The first false assumption is that a clean bill of lading proves product quality. It does not. It may show receipt of cargo by the carrier, but it does not inspect product workmanship or verify the AQL status of packed goods. The buyer still needs PSI before loading if product quality matters.

The second false assumption is that an intact seal proves quantity and condition. A seal can show that the container was not opened after sealing, but it does not prove the correct cartons were loaded or that cartons were undamaged at origin. Loading evidence fills that gap.

The third false assumption is that insurance automatically pays whenever goods arrive damaged. Claims depend on policy wording, cause of loss, documents, timing, survey evidence, and exclusions. A buyer who has better origin and arrival records is in a stronger position to explain what happened.

When Loading Inspection Is Worth Adding

Loading inspection is worth adding when loading mistakes would be hard to prove or expensive to correct after arrival.

Add loading inspection for high-value orders, retailer shipments, mixed-SKU containers, fragile goods, carton-sensitive packaging, seasonal inventory, products with pallet or stacking requirements, shipments from multiple production batches, and orders where supplier substitution risk exists.

It is also useful after a failed PSI that required rework. The buyer may want to verify that only corrected and accepted cartons are loaded. If the supplier corrected part of the lot and left rejected cartons nearby, loading supervision can help ensure the wrong cartons do not enter the container.

For Amazon FBA or retailer deliveries, loading evidence can support receiving conversations. It may not prevent every inbound issue, but it gives the buyer a cleaner origin record.

When Cargo Insurance Is Still Necessary

Insurance is still necessary because some transit risks cannot be inspected away.

Even perfectly inspected and properly loaded goods can be damaged or lost during transit. A container can be exposed to water, mishandled, delayed, stolen, or damaged in an accident. Loading inspection cannot compensate the buyer financially when a covered transit event occurs.

The buyer should review insured value, coverage type, deductible, excluded causes, claim deadline, documentation requirements, and who is named as insured. If the seller arranges insurance, the buyer should request policy evidence and understand whether coverage is adequate for the cargo and route.

The practical rule is simple: inspect what you can control before departure and insure what you cannot fully control during transit.

SPAR Scenario: Insurance Was Not Enough Without Loading Evidence

The claim conversation became harder because nobody documented carton condition at origin.

Situation: A U.S. importer ships a full container of boxed furniture from a Guangdong supplier. The buyer has cargo insurance but does not book loading supervision.

Problem: At arrival, several cartons are crushed and two SKUs are short. The supplier says the cartons were fine at loading. The forwarder says the container seal was intact. The warehouse photos show damage, but there is no origin evidence of container condition, carton condition, loading method, or loaded carton count.

Action: The buyer files a claim and also disputes the shortage with the supplier. The process is slow because the evidence record starts at arrival, not at loading.

Result: For the next order, the buyer keeps cargo insurance but adds container loading inspection after PSI. The loading report records carton count, container condition, loading sequence, and seal number, making later disputes much easier to handle.

Action Card: Transit Protection Plan

Do not choose between loading inspection and cargo insurance when the shipment needs both prevention and recovery.

- Use PSI to approve product quality before loading.

- Use container loading inspection to document the loading event, carton condition, quantity, and seal number.

- Buy cargo insurance appropriate to the cargo value, route, and risk.

- Confirm Incoterms, risk transfer, insurance obligations, and named insured status.

- Keep photos, videos, packing list, bill of lading, seal record, and arrival records together.

- Review claim procedure before the shipment moves, not after damage appears.

If your shipment is valuable, mixed-SKU, fragile, or retailer-bound, send TradeAider the packing list, container loading date, supplier location, PSI result, and cargo risk concerns. The next step is to ask TradeAider to add loading supervision after product acceptance.

Frequently Asked Questions

Does cargo insurance replace container loading inspection?

No. Cargo insurance may help recover money after a covered loss, while container loading inspection prevents and documents loading risk before departure.

Can loading inspection replace PSI?

No. PSI checks product quality before release; loading inspection checks container condition, carton condition, loading quantity, loading process, and seal evidence.

Do Incoterms decide whether I need insurance?

Incoterms help allocate responsibilities and, under CIF and CIP, include seller insurance obligations, but buyers still need to confirm whether coverage and evidence are adequate.

When should I book container loading inspection?

Book loading inspection after product quality is accepted and before the container is loaded, especially for high-value, fragile, mixed-SKU, or retailer-bound shipments.

Related Articles

Grow your business with TradeAider Service

Click the button below to directly enter the TradeAider Service System. The simple steps from booking and payment to receiving reports are easy to operate.